If you've tried to save money but always found it difficult, you might fare better if you create a budget – and stick to it. Creating a budget tells you what you can spend on a monthly basis. You can even create a weekly budget or break it down into a daily budget. Listing your expenditures helps you see where the money is going and where you can make cuts. The budget also shows how much you bring in and where you can pull from to grow your savings.

Figure Out Your Income

Not every month has four weeks, which means that your average monthly income is not the same. To determine your annual gross income, multiply your hourly wage by the number of hours you work each week, then multiply that amount by 52. If you are paid a salary, you should know how much you make per hour.

If not, get an average by dividing the gross amount on your weekly paycheck by 40, even if you work more or less than 40 hours. This will give you an hourly rate. If you are paid every two weeks, divide the gross amount by 80. If your employer pays you twice monthly, multiply the gross amount on your paycheck by 26 to get your yearly.

Figure out your yearly tax obligation using the same process. Subtract the annual tax obligation from your gross annual salary to get your net salary. Across the top of your budget, write down the yearly amounts for your gross pay, taxes and net pay.

Determine How You Want to Budget

Many people budget monthly, but you can choose any time frame. Divide your net, which also includes any other deductions such as retirement accounts and child support, by 12 if you want to do a monthly budget, by 52 if you're going to do a weekly budget, or by 26 if you're going to structure your budget around the 1st and the 15th of the month. These are the amounts you can spend during the allotted time frames.

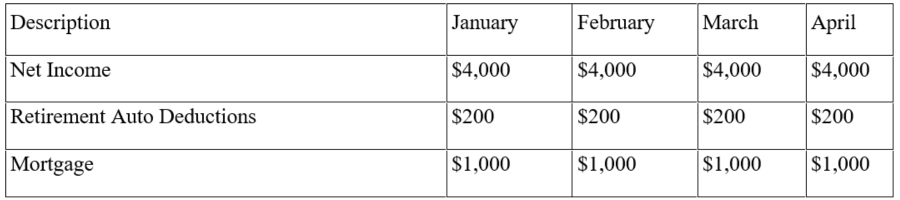

Create a Spreadsheet

If you don't want to use a pre-made budget planner, you can create a spreadsheet. It doesn't have to be anything fancy. You can use a spreadsheet program or just draw a spreadsheet on a piece of paper. The number of columns you use depends on how you structure your budget. A weekly budget will have 52 columns plus a description column. A monthly budget will have 12 plus the description column.

Continue listing your bills. You can add rows if you want to create subtotals between categories. For example, if you're going to list different sources of income separately, you can then create a "total" row to total your income. After any section, you can create an additional row to add them up and then yet another row to subtract them from your net income. Doing this allows you to see what you are already putting away or spending on necessary items such as child support, health insurance deducted from your paycheck and other deductions. The amount you have left is your adjusted net income.

Below all of that, create enough rows for your monthly bills. Fill in the spreadsheet. Subtract the total of your monthly bills from your net income or your net after deductions income. These should include any personal loans, vehicle loans, utilities, insurance premiums and other liabilities. This is what you have left after paying household bills.

Document Additional Expenditures

Start documenting additional expenditures in the order of importance to you. These should include gas, groceries, medications and other necessities. You can also include short-term liabilities, such as payments on retainer fees. Only list the obligations in this section. Starbucks is not a necessity! It's a good idea to total these expenditures with a separate row below this section, as this is where you may be able to cut back.

Document the Non-Necessary Items

Now comes the fun part. List everything you spend money on with regularity. This should include cigarettes, booze, Starbucks or your favorite coffee shop, eating out and entertainment. List "habit" items first, such as the morning trips to the coffee shop and, if you eat out at least once every week, eating out. Total these columns into a row.

Figure Out What's Left

Subtract all of your expenditures from your adjusted net income. What is left is what you should put into savings. If that amount is less than $20 per week and you make less than $30,000, you need to make cuts – enough so that you can save at least $50 per week. If you make at least $50,000, you should be able to save at least $50 per week, but you may want to get that amount to $100 per week by making cuts.

Set Up Savings and Debt Pay-Off Goals

In a second spreadsheet, set up your debt pay-off goals and savings goals. Every time you put extra money on a debt or make a deposit into your savings account, write it down – you'll get to see how much you're saving or paying down that debt. This not only serves as a reminder for you, but it also encourages you to do that as you watch your savings grow or your debt disappear.

Making Cuts

If you want to start contributing more to your savings or you want to pay off your house faster, you need to decide where you can cut expenses. Some suggestions include:

- Cable: Do you watch all the channels you subscribe to? Are many of them duplicates? For example, you might pay a separate fee for HBO and another for TMC. They often show the same movies. Consider getting rid of one of the packages. If you seldom watch movies on those channels, consider getting rid of all of them and switch to a streaming service or get rid of movie channels altogether.

- Eating Out: How often do you eat out? Once a week? Three times a week? Consider cutting that down to once every other week. Instead, plan weekly meals that fit your schedule. You can also make large meals and freeze them for later. Or, make part of it and freeze it. For example, instead of buying chicken pieces, buy a whole turkey. Cook it, divide what is left into meal-size portions and freeze it. The next time you want chicken or turkey, just thaw out a package of turkey. You can do this with ham, beef roasts and other larger cuts of meat.

- Coffee Shop Coffee: Getting a coffee at a high-end coffee shop every day starts adding up, especially when that cup of java pushes $5. If you do that five days per week, that's $25 per week or an average of $200 per month. Instead, buy your favorite coffee and make it yourself at least three times per week. You can also buy a cappuccino machine if you prefer cappuccino.

- Cell Phone: Do you use all of the data you pay for every month? If not, downgrade to a data plan that is more compatible with the amount of data you use.

- Groceries: Do you go shopping every day? Every other day? Plan your meals ahead of time, then go shopping once a week and buy food in bulk where you can. Invest in a chest freezer so that you can freeze meat and other food until you are ready to use it. You'll get a better price when you buy in bulk. Even those items you purchase that are not in bulk, such as fruits and veggies, will last a week in the refrigerator if stored properly. You'll save time and gas by not making that extra trip to the grocery store.

For every cut you make, add that much to your savings account. You'll be surprised at how much you are able to save every month!

Comments